For decades, the mantra of the property market has been “Location, Location, Location.” While a prime postcode will always hold sway, a new contender has entered the arena, fundamentally shifting how buyers, lenders, and conveyancers view property. That contender is Energy Efficiency.

Historically, the Energy Performance Certificate (EPC) was viewed by many sellers as a bureaucratic hurdle—a piece of paper to be filed away and forgotten during the conveyancing process. Today, however, amidst a backdrop of soaring energy prices, cost-of-living pressures, and increased climate awareness, the EPC has transformed from a tick-box exercise into a vital currency in the housing market.

For sellers, understanding the nuances of energy efficiency is no longer optional; it is a strategic necessity that impacts property value, mortgage saleability, and the speed of the legal transaction.

1. The EPC: From Paperwork to Price Point

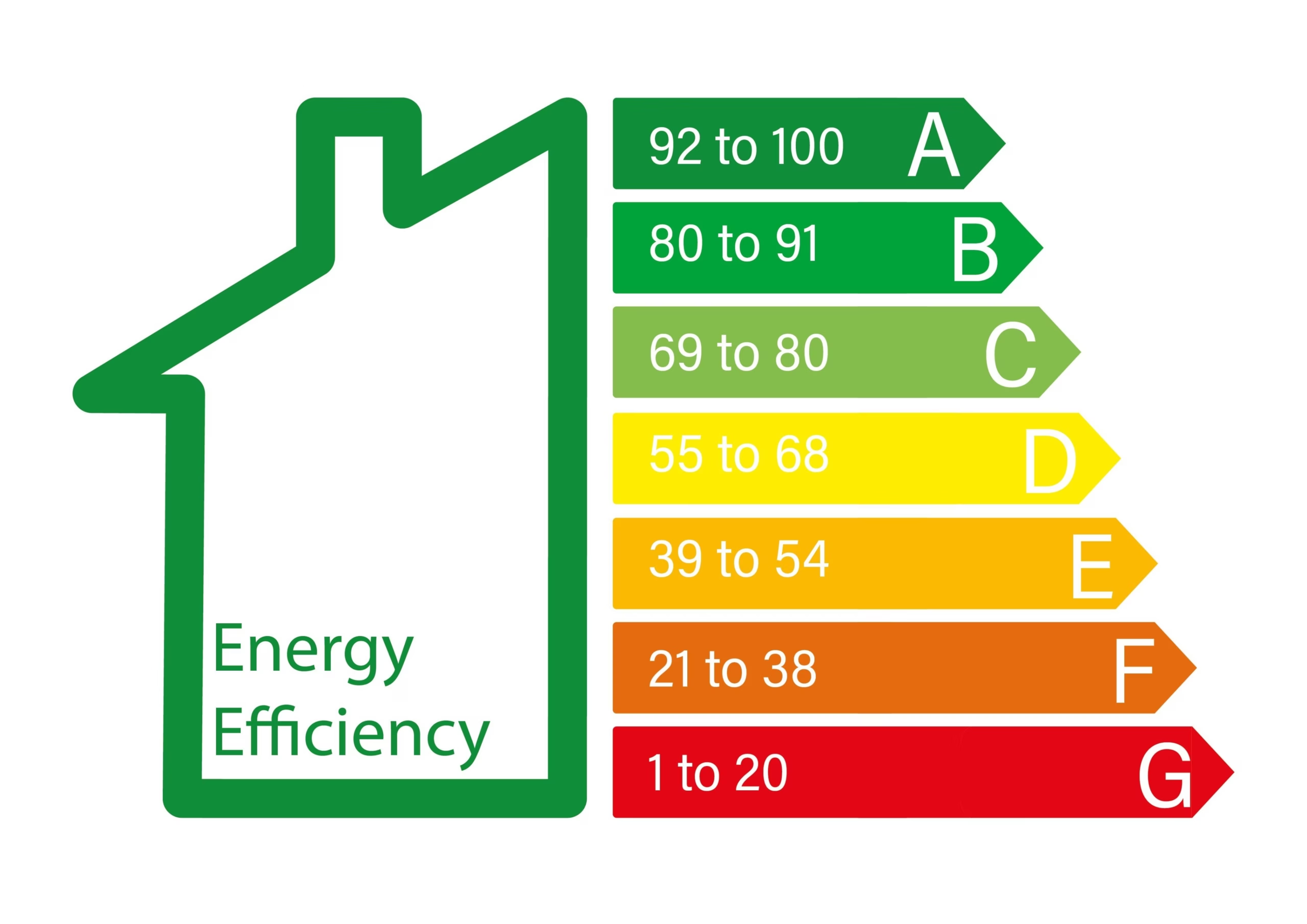

The Energy Performance Certificate rates a property from A (most efficient) to G (least efficient). It is a legal requirement to have a valid EPC when selling a property, and it is one of the first documents a conveyancer will request.

The “Green Premium” vs. The “Brown Discount”

In the current market, we are witnessing a bifurcation in property values.

-

The Green Premium: Homes with an EPC rating of C or above are increasingly commanding higher asking prices. Buyers are willing to pay more upfront for a “turnkey” energy-efficient home that promises lower monthly utility bills.

-

The Brown Discount: Conversely, properties rated D, E, F, or G are facing downward price pressure. Buyers view these properties as “projects” requiring significant capital injection to bring them up to modern standards.

In conveyancing terms, a poor EPC rating is becoming a frequent sticking point during pre-contract enquiries. Buyers’ solicitors are increasingly asking detailed questions about boiler age, insulation history, and window warranties. If an EPC reveals high projected running costs, buyers are now using this data to “gazunder” (lower their offer) just before the exchange of contracts, citing the cost of necessary retrofitting.

2. The Mortgage Landscape: Why Lenders Care

It isn’t just buyers scrutinising the energy efficiency of a home; it is the banks funding the purchase. The lending landscape is shifting rapidly towards “Green Finance.”

Green Mortgages

Many major lenders now offer specific “Green Mortgage” products. These products offer preferential interest rates or cashback incentives to borrowers purchasing homes with an EPC rating of A or B (and sometimes C).

-

For the Seller: If your home qualifies for a green mortgage, you effectively widen your pool of potential buyers. You become attractive to buyers who are specifically hunting for these lower interest rates.

-

For the Conveyancer: A green mortgage often comes with specific lending criteria. The conveyancer must verify the EPC rating against the lender’s requirements. If the rating on the certificate doesn’t match the lender’s stipulation, the mortgage offer can be withdrawn, causing the chain to collapse.

The Buy-to-Let (BTL) Squeeze

The impact is most acute in the investment sector. Under the Minimum Energy Efficiency Standards (MEES), it is currently unlawful to let a property with an EPC rating below E.

However, the government has long signaled intentions to raise this standard to a rating of C for new tenancies (potentially by 2028, though policy creates uncertainty). Consequently, landlords are offloading low-efficiency stock. If you are selling a property targeting investors, an EPC rating of D or E is a significant red flag. Investors will calculate the cost of bringing the property up to a C grade and deduct it from their offer, or their lender may simply refuse to finance the asset entirely.

3. Strategic Improvements: What Sellers Should Prioritise

If you are preparing to sell, you might be tempted to overhaul the entire property. However, not all energy improvements offer a good Return on Investment (ROI) when you are about to leave.

The goal is to improve the EPC rating and visual appeal without overcapitalising. Here is a tiered approach to prioritising upgrades.

Tier 1: The “Quick Wins” (Low Cost, High Appeal)

Before you list the property, ensure you have addressed the basics. These fix the “optics” of the home.

-

Lighting: Replace all halogen or incandescent bulbs with LEDs. It is a cheap fix that marginally improves the EPC score but significantly improves the modern feel of the home.

-

Draft Proofing: Seal gaps around windows, doors, and letterboxes. While this doesn’t always dramatically shift the EPC number, it changes the feeling of the viewing. A drafty home feels cold and expensive; a sealed home feels well-maintained.

-

Jacket the Tank: If you have a hot water cylinder, ensure it has a thick insulating jacket (at least 80mm). This is one of the cheapest points to gain on an EPC.

Tier 2: The “Smart Investments” (Medium Cost, Best ROI)

These are the upgrades that generally pay for themselves by moving a property from a D to a C rating.

-

-

Loft Insulation: This is the single most effective upgrade for cost vs. impact. If you have less than 270mm of loft insulation, top it up.

-

Conveyancing Tip: Keep the receipt and guarantee. The buyers’ solicitor will ask for evidence of when this was done.

-

-

-

Cavity Wall Insulation: If your home has cavity walls that haven’t been filled, this can significantly jump your EPC score.

-

Thermostatic Radiator Valves (TRVs): Installing TRVs allows heating control for individual rooms. It shows buyers that the heating system is controllable and efficient, even if the boiler isn’t brand new.

Tier 3: The “Cautionary Upgrades” (High Cost)

Be careful with big-ticket items. You are unlikely to get your money back 1-for-1 on the sale price, so only do these if necessary to secure a sale or if the current system is broken.

-

-

Double/Triple Glazing: If you have single glazing, it is a major devaluation factor. However, upgrading from older double glazing to new triple glazing is rarely worth the cost purely for a sale.

-

Heat Pumps: While excellent for long-term owners, installing a heat pump is expensive and disruptive. Most buyers would prefer a standard, working boiler and the option to install a heat pump later.

-

Solar Panels: These add value, but the payback period is 10-15 years. Install them if you plan to stay; be cautious if you plan to sell next year.

-

4. The Conveyancing Checklist for Energy Efficiency

As a seller, you can speed up your conveyancing process by being proactive regarding energy documentation. A delay in providing certificates is a common cause of friction in the weeks leading up to the exchange.

Before you list your home, prepare the following:

-

The EPC: Ensure it is current (they last 10 years) and reflects the current state of the property. If you have added a new boiler or insulation since the last EPC, get a new assessment done. A £100 assessment could add thousands to the value by pushing you into a higher band.

-

FENSA/CERTASS Certificates: If you have replaced windows, you must have the building regulation compliance certificates.

-

Boiler Service History: A fully serviced boiler suggests an efficient boiler. Gaps in service history make buyers nervous about efficiency and safety.

-

Guarantees: Paperwork for cavity wall insulation or solar panels must be ready for the buyer’s solicitor immediately.

Summary

Energy efficiency is no longer just about saving the planet; it is about preserving the equity in your home.

In the modern conveyancing landscape, a poor EPC rating acts as a drag on transaction speed and a chip away at the sale price. By understanding how mortgage lenders view efficiency and prioritising the right improvements—specifically insulation and heating controls—sellers can protect their property value and ensure a smoother ride from offer to completion.

Don’t let your sale freeze over because of a cold house. Check your EPC today, and make the changes that matter.